Satisfy the Extended Island fellas who adore unloved purchasing malls

Igal Namdar and Elliot Nassim 1st teamed up a decade in the past to obtain difficulty U.S. searching malls.

Now they rank amongst the biggest all-hard cash purchasers of the nation’s challenging-luck malls. The pandemic has manufactured it even harder for shopping mall home proprietors presently struggling to preserve up on home loan payments, resulting in numerous significant players throwing in the towel on distressed qualities and with additional very likely.

The duo, by Namdar Realty Team and Mason Asset Management out of Great Neck, Lengthy Island, now owns about 60 million sq. ft of buying centre place, which include around of 100 open-air qualities are 65 enclosed malls. That kind of footprint puts them in league with Macerich Co.

MAC,

and other main mall owners with a coastline-to-coastline get to.

As an alternative of U.S. stockholders and quarterly reports, the group keeps things straightforward: Namdar focuses on administration facet of the houses. Nassim handles leasing and asset administration. Namdar, by Namco Realty Ltd, also a couple years back raised thousands and thousands in Israel by offering bonds tied to his houses.

But what definitely sets them aside is a steady stream of all-dollars offers to sellers who want out. In return, they want a price reduction.

“We see that a good deal of these malls are staying offered by creditors,” reported Igal Namdar, the company’s president, in an interview with MarketWatch. “And the surety of near is an critical matter for them.”

“We see that becoming in a position to near all-income, normally times receives you a lower price from wherever the current market it,” he stated. “That is wherever we form of make our money.”

A number of industry experts pointed to Nadmar and Nassim as among the sector’s largest dollars shopping mall buyers. “I would say that we almost certainly bid on a lot more malls than any other company,” Namdar stated.

Bloomberg Information not long ago noted on authorized problems stemming from the “bottom feeder” technique, when pegging Namdar’s particular net value at around $2 billion.

Namdar declined to comment on that net value estimate when requested by MarketWatch. “While we can’t comment on matters of energetic litigation, we do take any lawsuits towards our crew quite critically,” the group advised MarketWatch. “It is always our objective to incorporate worth to our houses, and we are diligent in our initiatives to cure any upkeep or administration situation that is introduced to our attention.”

In a nutshell, theirs is a wager that any mall can produce a financial gain, if the rate paid is much less than money coming in from tenant leases. If some previous malls can be used in new, innovative strategies, these as the “mini-casino” strategy for an aged Macy’s shop at Namdar-owned Nittany Mall in Point out Faculty, Penn, all the better.

Billions on the line

The economical issues tied to struggling U.S. malls previously runs into the billions.

About $4.6 billion of U.S. purchasing heart financial debt has been pegged to possible deed-in-lieu of foreclosures gatherings, liquidations or genuine estate owned (REO) houses, in accordance to a checklist compiled by Invoice Petersen, co-founder of CREDiQ, a commercial authentic estate analytics company.

An REO assets is 1 the place a residence is owned by a lender because it failed to promote in a foreclosure auction immediately after the borrower defaulted on the home finance loan.

Mainly because numerous properties remain in limbo, the worst of the disaster for mall home loan bond traders probably has however to occur.

Roughly $3 billion searching shopping mall loans in professional home finance loan bond specials have been determined as at-chance of becoming handed again to loan companies, in accordance to investigation business and information tracker Trepp.

“I assume some mall proprietors will muddle by way of with the assist of loan modifications and maybe some peripheral credit card debt forgiveness,” said Manus Clancy, senior handling director and head of investigate at Trepp. “Others will be handed again to loan companies through an uncontested or confrontational foreclosure course of action.”

The Drano for Underwater Malls

A great deal has been created about the demise of American shopping mall, such as a short while ago by the New York Periods in an report that notes the “deep nostalgia” many men and women have for local malls, even as lots of home homeowners have been having difficulties for many years to retain the lights on.

Morgan Stanley’s retail team of analysts forecast last October that the pandemic could drive 35% of U.S. procuring malls to shut forever. Trillions of pounds value of fiscal and monetary stimulus by the federal govt and Federal Reserve served staunch the carnage, with only 13 malls so considerably this yr trading to new homeowners.

Namdar and Nassim could help to unclog the debt backlog of underwater mall attributes.

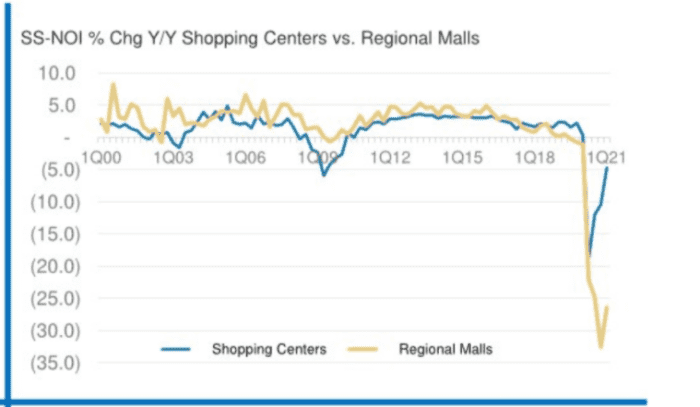

In section, which is mainly because financials could proceed to head downhill for a lot of lower-top quality mall proprietors. Regional malls viewed same-store net functioning profits plunge on normal by minus 26.1% in the to start with quarter from a calendar year back, in accordance to Morgan Stanley.

Malls see net functioning money plunge

Morgan Stanley Investigation

Lifting of pandemic constraints in the latest months has been a boon for shares of leading shopping mall operators like Simon Assets Group

SPG,

and Kimco Realty Corp.

KIM,

each up a lot more than 40% on the yr so significantly. That compares with a 18.4% attain for the S&P 500 Index

SPX,

for the calendar year as of Tuesday, even though the Dow Jones Industrial Average

DJIA,

was up 15.4%.

The surge in retail REIT shares comes regardless of a backdrop of significant-photograph worries, not only from slumping retail rents and occupancy stages, but also a crush of tenant leases coming thanks more than the up coming a few to four yrs.

That’s when Morgan Stanley’s crew estimates that 50% of shopping mall-primarily based specialty leases, including all those of American Eagle Outfitters Inc.

AEO,

the Hole Inc

GPS,

and some others, occur up for renewal.

The pandemic also isn’t over nevertheless, which include in the U.S., exactly where COVID hospitalizations have been climbing, despite common availability of vaccines for adults, raising problems close to the recovery.

The government’s release Tuesday of July U.S. retail product sales confirmed a sharp 1.1% fall on a regular basis, underscoring anxieties tied to the delta variant of the coronavirus, but also a shift in priorities from “goods to products and services,” James Knightley, ING’s main international economist, wrote in emailed opinions.

The attributes Namdar and Nassim began scooping up soon after the 2008 financial disaster had been “C” or “D” malls, classes, like test grades, that stage to area for enhancement or around failure. These days, the staff has been moving up in excellent.

“We are a very low leverage company. And we are out there looking all the time for prospects to acquire improved belongings than when we initially commenced,” Namdar instructed MarketWatch. “As we make our portfolio, we want to continually make improvements to the high-quality by having greater belongings.”

No 1 doubts the best U.S. malls will endure — and even thrive — the moment the pandemic carnage plays out, mentioned Daniel McNamara, a principal at MP Securitized Credit Associates. But he continue to sees the trouble as far too a great deal debt on decreased high quality houses financed decades ago, when shopping mall valuations ended up pegged at a lot bigger ranges.

“The Class A operators are executing excellent,” McNamara advised MarketWatch. “But almost anything at all beneath ‘Class A,’ there really has been no bid for, besides for the Namdar’s of the planet. And it has to be all cash.”

Like billionaire Carl Icahn, McNamara’s hedge fund has been betting on the personal debt of more mature malls heading negative.

BofA Global’s research group lately place it this way, “while on the web buying experienced previously been cannibalizing brick and mortar retail, the pain felt by many retailers prior to Covid was exacerbated through the pandemic,” in a weekly take note.

Significant browsing mall proprietors, which include Simon Property, Starwood Capital, Brookfield Asset Management and other individuals have reacted to the upheaval by handing again the keys to creditors on some qualities, relatively than “throw excellent money” immediately after undesirable.

Browse: Brookfield to hand back again keys to a few malls, probably much more, as it goes private in $6.5 billion deal

The Inexperienced Street Commercial Residence Value Index has mall values down 18% due to the fact just before the pandemic.

The Namdar staff hopes far more, larger top quality malls will keep shaking free.

“During the pandemic, there have been a lot less offers out there,” Namdar stated, incorporating that most creditors have been doing work with their debtors, but also that many have been unwilling “to take a significant create off yet.”

“But we are advised in the up coming yr or 18 months, there will be a large amount of specials coming to the market place,” he mentioned.